Resources & Links

-

Home Financing: PEWHousing is the largest regular expense for most American families. And although prices vary significantly across the nation, living in a lower-cost area does not always ease the path to homeownership. Many families in less expensive regions struggle to buy a home because small mortgages are hard to obtain.

-

Blacks and Hispanics face extra challenges in getting home loansHomeownership in the U.S. has fallen sharply since the housing boom peaked in the mid-2000s, though it’s declined more for some racial and ethnic groups than for others. Black and Hispanic households today are still far less likely than white households to own their own homes (41.3% and 47%, respectively, versus 71.9% for whites), and the homeownership gap between blacks and whites has widened since 2004.

-

Mortgage Terms: What You Need To KnowThe average homeowner lives in a home for 10 years, according to the 2019 Profile of Home Buyers and Sellers from the National Association of Realtors. This means that, not counting refinances, the typical homeowner is exposed to mortgage jargon once each decade.

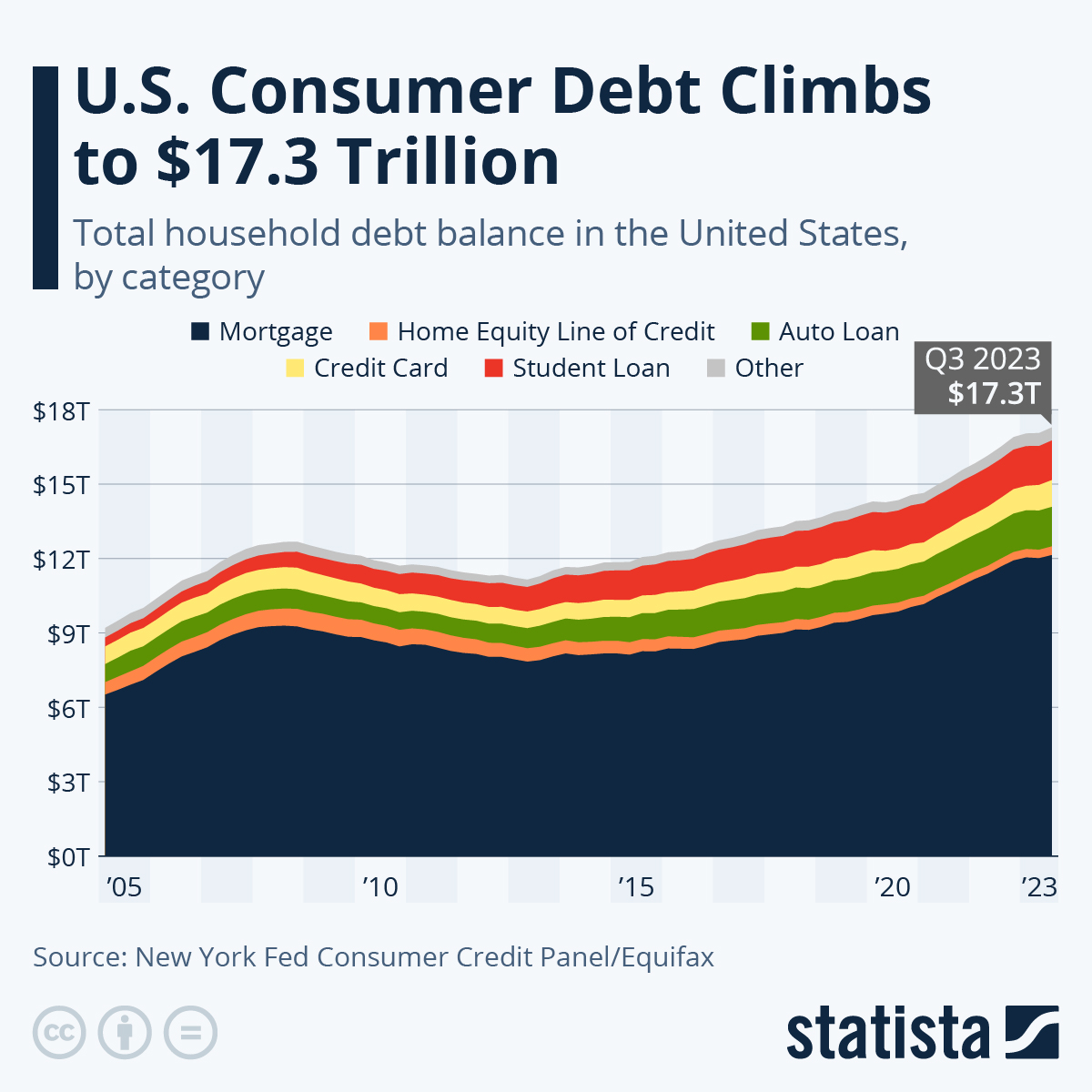

Driven by Mortgages, U.S. Household Debt Hits New High

You will find more infographics at Statista

You will find more infographics at Statista

Perspectives

Regaining the Dream

Millions of Americans have lost their homes since the start of the recession initiated by the financial crisis of 2008-09. But is the dream of homeownership for America's working families obsolete, an aspiration from a bygone era? Regaining the Dream rejects that notion and proposes a way to strengthen the financial system while simultaneously promoting an equitable and viable American homeownership policy. For the first time, the authors of Regaining the Dream offer data-driven evidence on how the mortgage industry can serve working families in the United States, pointing the way to a pragmatic housing policy that promotes the opportunity for sustainable homeownership. Taking the reader step by step through the lending crisis and what caused it, the authors include useful and clear definitions of terms heard almost daily in news coverage. And they give a fair account of the history behind Fannie Mae and Freddie Mac and the new Dodd-Frank law, explaining what remains to be done to uphold one of the defining characteristics of the American dream.

Race for Profit: How Banks and the Real estate Industry Undermined Black Homeownership

LONGLISTED FOR THE 2019 NATIONAL BOOK AWARD FINALIST, 2020 PULITZER PRIZE IN HISTORY By the late 1960s and early 1970s, reeling from a wave of urban uprisings, politicians finally worked to end the practice of redlining. Reasoning that the turbulence could be calmed by turning Black city-dwellers into homeowners, they passed the Housing and Urban Development Act of 1968, and set about establishing policies to induce mortgage lenders and the real estate industry to treat Black homebuyers equally. The disaster that ensued revealed that racist exclusion had not been eradicated, but rather transmuted into a new phenomenon of predatory inclusion. Race for Profit uncovers how exploitative real estate practices continued well after housing discrimination was banned. The same racist structures and individuals remained intact after redlining's end, and close relationships between regulators and the industry created incentives to ignore improprieties. Meanwhile, new policies meant to encourage low-income homeownership created new methods to exploit Black homeowners. The federal government guaranteed urban mortgages in an attempt to overcome resistance to lending to Black buyers - as if unprofitability, rather than racism, was the cause of housing segregation. Bankers, investors, and real estate agents took advantage of the perverse incentives, targeting the Black women most likely to fail to keep up their home payments and slip into foreclosure, multiplying their profits. As a result, by the end of the 1970s, the nation's first programs to encourage Black homeownership ended with tens of thousands of foreclosures in Black communities across the country. The push to uplift Black homeownership had descended into a goldmine for realtors and mortgage lenders, and a ready-made cudgel for the champions of deregulation to wield against government intervention of any kind. Narrating the story of a sea-change in housing policy and its dire impact on African Americans, Race for Profit reveals how the urban core was transformed into a new frontier of cynical extraction.

The Rise and Fall of the US Mortgage and Credit Markets

The mortgage meltdown: what went wrong and how do we fix it? Owning a home can bestow a sense of security and independence. But today, in a cruel twist, many Americans now regard their homes as a source of worry and dashed expectations. How did everything go haywire? And what can we do about it now? In The Rise and Fall of the U.S. Mortgage and Credit Markets, renowned finance expert James Barth offers a comprehensive examination of the mortgage meltdown. Together with a team of economists at the Milken Institute, he explores the shock waves that have rippled through the entire financial sector and the real economy. Deploying an incredibly detailed and extensive set of data, the book offers in-depth analysis of the mortgage meltdown and the resulting worldwide financial crisis. This authoritative volume explores what went wrong in every critical area, including securitization, loan origination practices, regulation and supervision, Fannie Mae and Freddie Mac, leverage and accounting practices, and of course, the rating agencies. The authors explain the steps the government has taken to address the crisis thus far, arguing that we have yet to address the larger issues. Offers a comprehensive examination of the mortgage market meltdown and its reverberations throughout the financial sector and the real economy Explores several important issues that policymakers must address in any future reshaping of financial market regulations Addresses how we can begin to move forward and prevent similar crises from shaking the foundations of our financial system The Rise and Fall of the U.S. Mortgage and Credit Markets analyzes the factors that should drive reform and explores the issues that policymakers must confront in any future reshaping of financial market regulations.

Guaranteed to Fail:Fannie Mae, Freddie Mac, and the Debacle of Mortgage Finance

Why America's public-private mortgage giants threaten the world economy--and what to do about it The financial collapse of Fannie Mae and Freddie Mac in 2008 led to one of the most sweeping government interventions in private financial markets in history. The bailout has already cost American taxpayers close to $150 billion, and substantially more will be needed. The U.S. economy--and by extension, the global financial system--has a lot riding on Fannie and Freddie. They cannot fail, yet that is precisely what these mortgage giants are guaranteed to do. How can we limit the damage to our economy, and avoid making the same mistakes in the future? Guaranteed to Fail explains how poorly designed government guarantees for Fannie Mae and Freddie Mac led to the debacle of mortgage finance in the United States, weighs different reform proposals, and provides sensible, practical recommendations. Despite repeated calls for tougher action, Washington has expanded the scope of its guarantees to Fannie and Freddie, fueling more and more housing and mortgages all across the economy--and putting all of us at risk. This book unravels the dizzyingly immense, highly interconnected businesses of Fannie and Freddie. It proposes a unique model of reform that emphasizes public-private partnership, one that can serve as a blueprint for better organizing and managing government-sponsored enterprises like Fannie Mae and Freddie Mac. In doing so, Guaranteed to Fail strikes a cautionary note about excessive government intervention in markets.

The Great American Housing Bubble: the Road to Collapse

In the aftermath of the American housing collapse in 2007, many ask why. The Great American Housing Bubble: The Road to Collapse asks a different and more fundamental question--how the bubble was created in the first place. To answer that question, it examines the causes, both political and economic, of the American housing bubble, created between 1940 and 2007. Those causes encompass everything from federal income tax subsidies for housing to local exclusionary policies, banking, accounting, real estate appraisal, and credit agency rating practices and policies. The book also takes into account the impact of greed, government regulation, speculation, and psychology--including blind faith in investment advisors--on the creation of the greatest asset bubble in the economic history of the world. The author takes a comparative historical approach, examining the current crisis in the light of notorious bubbles of the past. In the end, he concludes that the events precipitating the most recent collapse can be traced, at least in part, not to too little government regulation, but to too much.

Streaming Media

-

Why Do Millions of U.S. Homebuyers Use Risky Financing Options?Homes come in all shapes and sizes—and so do the loans needed to buy them. For many prospective buyers, obtaining a traditional, safe 15- or 30-year mortgage is a key step to achieving financial security and their dream of homeownership.